12 May What Assets Are Exempt from Medicaid in Illinois? 2026 Guide

If you are helping a parent or spouse apply for Medicaid in Illinois, one of the first questions is usually simple:

What can they keep?

Families often worry that Medicaid will require a parent to lose everything before help is available. That is not exactly how the rules work. Illinois Medicaid looks at countable assets, but some assets may be exempt, meaning they are not counted against the Medicaid asset limit.

For many families, the key is understanding the difference between assets that count, assets that may be exempt, and assets that may be protected with the right planning.

In 2026, the Illinois asset limit for Aged, Blind, and Disabled Medical cases is generally $17,500 in non-exempt resources. Illinois DHS states that the medical asset limit is $17,500, and the 2026 Illinois Medicaid standards chart also lists AABD Medical resources/assets at $17,500.

That does not mean a person can only own $17,500 in total. Some property may not count toward the limit.

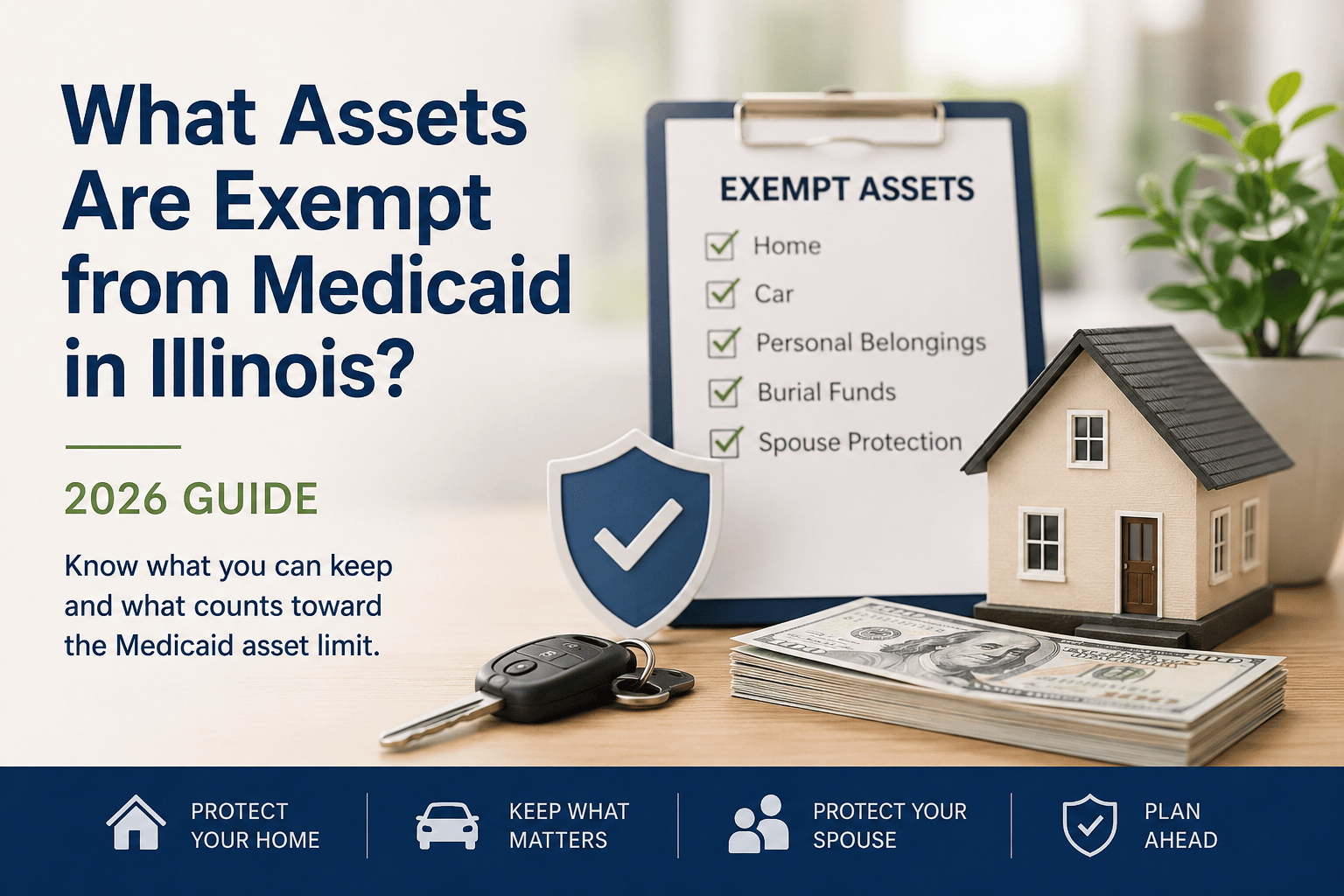

Quick Answer: What Assets May Be Exempt from Medicaid in Illinois?

In Illinois, common exempt or partly exempt assets may include:

| Asset | Usually Exempt? | What Families Should Know |

|---|---|---|

| Primary home | Sometimes | The home may be exempt for eligibility, but estate recovery can still be an issue later. |

| One vehicle | Often | One car is commonly treated differently from extra vehicles. |

| Personal belongings | Usually | Clothing, furniture, and household items are generally not the main issue. |

| Burial spaces | Usually | Burial plots and related arrangements may be exempt. |

| Certain burial funds | Sometimes | The details matter. How the money is held can change the result. |

| Some life insurance | Sometimes | Term life and small or certain policies may be treated differently from policies with cash value. |

| Spouse’s protected assets | Partly | If one spouse needs long-term care, special spousal impoverishment rules may apply. |

| Bank accounts | Usually countable | Cash, checking, and savings accounts usually count. |

| Investments | Usually countable | Stocks, bonds, CDs, brokerage accounts, and similar assets usually count. |

| Second home | Usually countable | Vacation homes, rental properties, and extra real estate need careful review. |

Illinois Legal Aid describes exempt resources as typically including a person’s home, a single car, personal belongings, some life insurance policies, burial spaces, and more.

What Does “Exempt Asset” Mean?

An exempt asset is property that Medicaid does not count against the applicant’s asset limit.

A countable asset is property that Medicaid does count.

This distinction matters because a person may be over the asset limit on paper, but still qualify if much of what they own is exempt. For example, a person may own a modest home, one car, furniture, clothing, and a small bank account. The home and car may not create the same issue as cash in a savings account.

The problem for many families is that the rules are not always obvious. The home may be exempt in one situation and risky in another. A life insurance policy may be harmless in one case and countable in another. A transfer to a child may seem logical but create a Medicaid penalty.

That is why families should review the asset picture before applying, especially when a home, trust, gift, spouse, or nursing home is involved.

Illinois Medicaid Asset Limit in 2026

For many older adults applying under Illinois AABD Medical rules, the key resource limit is $17,500 in non-exempt assets. Illinois DHS says the medical asset limit is $17,500, and that this applies whether one person or more is in the household.

Illinois Aging’s 2026 Medicaid chart also lists AABD Medical resources/assets at $17,500.

This is where families often get confused. The limit applies to non-exempt resources. It does not automatically include every single thing the person owns.

A simple way to think about it:

- Exempt assets may be allowed.

- Countable assets are measured against the asset limit.

- Transfers and gifts may trigger separate Medicaid lookback rules.

- Estate recovery may still affect property after death, even if the asset was exempt during life.

Countable Assets vs Exempt Assets

The first step is to separate assets into two groups.

Assets that usually count

These often include:

- Cash

- Checking accounts

- Savings accounts

- Certificates of deposit

- Stocks

- Bonds

- Brokerage accounts

- Mutual funds

- Some life insurance cash value

- Extra vehicles

- Second homes

- Vacation property

- Some rental property

- Money owed to the applicant

- Assets held jointly with others, depending on ownership and access

Assets that may be exempt

These may include:

- A primary residence, depending on the facts

- One vehicle

- Household goods

- Personal belongings

- Burial spaces

- Certain burial arrangements

- Some life insurance policies

- Some assets used to produce income

- Certain assets protected for a spouse

The word “may” matters here. Medicaid rules depend on the type of Medicaid, the applicant’s living situation, marital status, ownership structure, and timing.

Is the Home Exempt from Medicaid in Illinois?

The home is usually the asset families care about most.

In many cases, a primary residence may be treated as exempt for Medicaid eligibility. This can be true where the applicant still lives in the home, intends to return home, or has a spouse or certain dependent or disabled relatives living there.

The 2026 Illinois Medicaid standards chart lists a home equity limit of $752,000.

That means the home should not be treated casually. A home can be exempt for one purpose and still create issues later.

There are three separate questions families should ask:

- Will the home count against Medicaid eligibility?

- Could Medicaid recover against the home after death?

- Is there a legal way to protect the home before a crisis?

Those are not the same question.

A parent may qualify for Medicaid while still owning a home. That does not always mean the home is fully protected from future estate recovery.

Illinois HFS explains that Medicaid estate recovery may apply after death, although there are limits and exceptions. For estates of Medicaid customers with a date of death on or after July 1, 2022, Illinois allows no recovery against the first $25,000 of estate value. HFS also lists situations where the state will not ask for recovery, including where there is a surviving spouse, a child under 21, or a child of any age who is blind or permanently and totally disabled under Social Security requirements.

Is One Car Exempt from Medicaid?

In many Medicaid cases, one vehicle is not treated the same way as cash or investments.

This matters because a car is often necessary for the spouse at home, family support, medical appointments, shopping, and daily life.

Illinois Legal Aid includes a single car among the typical exempt resources for AABD Medicaid.

That does not mean every vehicle is ignored. Extra vehicles, collectible vehicles, or vehicles with unusual value may need a closer look.

For most families, the first car is not the issue. The bigger issue is usually cash, savings, investment accounts, extra real estate, or transfers made before the Medicaid application.

Are Personal Belongings and Household Goods Exempt?

Most ordinary personal belongings and household goods are not the focus of Medicaid planning.

This includes things like:

- Clothing

- Furniture

- Beds

- Kitchen items

- Basic electronics

- Family photos

- Normal household contents

Illinois Legal Aid includes personal belongings among the resources that are typically exempt.

Families generally do not need to panic about ordinary household items. The more serious issues are usually bank accounts, property, investments, trusts, prior gifts, and ownership records.

Are Burial Funds or Funeral Arrangements Exempt?

Certain burial spaces and some funeral or burial arrangements may be exempt.

This can include burial plots and related arrangements. Illinois Legal Aid includes burial spaces among typical exempt resources.

Families should be careful with this area because the structure matters. A prepaid funeral arrangement, burial account, or life insurance-funded burial plan can be treated differently depending on how it is set up.

Before moving money into a burial plan, families should check whether it will be treated as exempt and whether it creates any transfer or access issue.

Does Life Insurance Count as an Asset?

Life insurance needs careful review.

Some life insurance policies may not count, while others may have cash value that Medicaid considers available. Illinois DHS gives the cash value of a nonexempt life insurance policy as an example of something that can be part of the asset limit.

A term life policy is different from a whole life policy with cash value. A small policy may be treated differently from a larger one. Beneficiary designations can also matter for estate recovery and family planning.

Families should gather:

- The policy type

- The death benefit

- The cash surrender value

- The owner

- The insured person

- The beneficiary

- Any loans against the policy

This information should be reviewed before assuming the policy is safe or problematic.

What Assets Can a Spouse Keep in Illinois?

Married couples have special rules when one spouse needs long-term care and the other spouse remains in the community.

The spouse who remains at home is often called the community spouse. The spouse applying for or receiving long-term care Medicaid may be called the LTC spouse.

For 2026, Illinois HFS says the Community Spouse Resource Allowance standard changed to $143,172. This is the maximum amount of resources a resident may transfer to a community spouse or for the sole benefit of a community spouse, subject to the actual calculation.

Illinois DHS also states that the CSRA, up to $143,172, is not considered available to pay for the care of the LTC spouse for applications received on or after January 1, 2026.

This is one of the most important protections in Medicaid planning.

It can help prevent the healthy spouse from being left with too little to live on. It can also create planning options that are not available in a single-person case.

What Assets Usually Count Toward the Medicaid Limit?

The assets that usually cause problems are the assets that can be easily converted to cash or used to pay for care.

These often include:

- Checking accounts

- Savings accounts

- Cash

- CDs

- Stocks

- Bonds

- Mutual funds

- Brokerage accounts

- Extra vehicles

- Second homes

- Vacation property

- Some rental property

- Some life insurance cash value

Families should also be careful with joint accounts. Adding a child’s name to an account does not automatically solve the issue. Medicaid may still treat the funds as available, depending on the facts.

The same is true for property deeds. Transferring a home to a child can create serious Medicaid problems if it is done during the lookback period.

Can You Give Assets Away Before Applying for Medicaid?

This is one of the most common and most dangerous mistakes.

Families sometimes think they can give assets to children and then apply for Medicaid. For long-term care Medicaid, that can trigger the 5-year lookback period.

Illinois Legal Aid explains that if someone applying for Medicaid long-term care transferred property for less than fair market value during the last five years, they may be ineligible for long-term care Medicaid for a period of time.

That penalty can be very hard on a family because it may arise when care is already needed.

The timing matters. The amount transferred matters. The reason for the transfer matters. The type of asset matters.

Before gifting money, transferring a deed, changing account ownership, or moving assets into a trust, families should get advice.

Is a Trust an Exempt Asset?

A trust is not automatically exempt.

This is another area where families can get into trouble. The name of the trust is not enough. Medicaid will look at the terms, timing, control, access, and whether the trust was funded correctly.

A revocable living trust usually does not protect assets from Medicaid because the person who created it often still has access and control.

An irrevocable Medicaid Asset Protection Trust may help in some situations, but it usually needs to be created and funded well before care is needed. The 5-year lookback still matters.

A trust that is drafted incorrectly, funded too late, or misunderstood can fail to provide the protection the family expected.

Example 1: Single Parent With a Home and Savings

Mary is 82 and lives in Glenview. She owns her home, has one car, and has $42,000 in a savings account.

Her home and car may not be the main eligibility problem. The $42,000 savings account is more likely to create an issue because it is a countable resource.

Mary’s family should not assume she needs to spend everything quickly. Some spending may be appropriate. Some planning may be available. Some mistakes could create penalties.

The right question is not simply, “How do we get below the asset limit?”

The better question is:

What can be preserved, what must be spent, and what needs to be handled before applying?

Example 2: Married Couple With One Spouse Entering a Nursing Home

John needs nursing home care. His wife, Anne, still lives at home.

They own their home, one car, and have $180,000 in combined savings and investments.

This is not the same as a single-person case. Anne may be able to keep a protected amount under the community spouse rules. In 2026, Illinois uses a CSRA standard of $143,172.

The couple may also have income issues to review. The goal is to help John qualify for care without leaving Anne financially exposed.

This type of case should be reviewed carefully before assets are spent or transferred.

Example 3: Adult Children Added to a Bank Account

A father adds his daughter to his bank account so she can help pay bills.

Later, he needs nursing home care and applies for Medicaid.

The family may think half the account belongs to the daughter. Medicaid may not see it that way. The result can depend on where the money came from, who had access, how the account was titled, and what records exist.

Joint ownership can be useful for convenience, but it does not always protect the asset.

Example 4: Transferring the House to the Children

A mother signs her house over to her children because she heard Medicaid cannot take what she does not own.

Two years later, she needs nursing home care.

That transfer may create a Medicaid penalty because it occurred within the 5-year lookback period. The family may also have created tax, ownership, creditor, or family conflict issues.

A deed transfer should not be done casually. There may be better planning tools, but the right option depends on timing and family circumstances.

Should You Spend Down Assets or Protect Them?

Spenddown can be part of Medicaid planning, but it should be done carefully.

Permitted spending may include things like:

- Paying legitimate debts

- Making home repairs

- Purchasing needed medical equipment

- Paying for care

- Buying exempt items

- Setting up appropriate burial arrangements

- Legal planning

Poorly planned spenddown can waste money or create new problems.

For example, a family might spend money on things that do not improve the parent’s care, fail to protect the spouse, or transfer assets in a way that creates a penalty.

The goal should be practical:

Qualify for the right care while preserving as much stability, dignity, and family security as the law allows.

When Should You Speak With an Elder Law Attorney?

You should consider speaking with an Illinois elder law attorney before applying for Medicaid if:

- A parent owns a home

- A spouse still lives at home

- There is more than $17,500 in countable assets

- Money was gifted in the last five years

- A deed was changed

- A trust exists

- A parent is already in a nursing home

- A parent may need nursing home care soon

- The family is unsure what Medicaid will count

- You want to protect the home from future estate recovery

At ElderSmart, Martin Fogarty helps Illinois families understand these rules before they make costly mistakes. Martin has worked in elder law, estate planning, and related legal planning for more than 30 years. His approach is shaped by professional experience and by his own family’s experience with the decline of a loved one from Alzheimer’s.

The goal is to give families clear answers, practical options, and a plan that protects the person who needs care without ignoring the spouse, children, or home they worked hard to build.

FAQ: Exempt Assets and Medicaid in Illinois

What is the Medicaid asset limit in Illinois in 2026?

For many Aged, Blind, and Disabled Medical cases in Illinois, the asset limit is $17,500 in non-exempt resources. Illinois DHS lists the medical asset limit at $17,500, and Illinois Aging’s 2026 Medicaid chart also lists AABD Medical resources/assets at $17,500.

Does Medicaid count your house in Illinois?

A primary home may be exempt for eligibility in some cases, especially if the applicant lives there, intends to return, or has a spouse or certain protected relatives living there. That does not mean the home is always safe from estate recovery after death.

Can Medicaid take your house after death in Illinois?

Illinois may pursue Medicaid estate recovery after death in some cases. HFS says recovery does not apply to the first $25,000 of estate value for Medicaid customers with a date of death on or after July 1, 2022. HFS also lists exceptions, including a surviving spouse, a child under 21, or a child of any age who is blind or permanently and totally disabled under Social Security rules.

Is one car exempt from Medicaid in Illinois?

Often, yes. Illinois Legal Aid includes a single car among the typical exempt resources for AABD Medicaid. Extra vehicles or unusually valuable vehicles may need review.

Are bank accounts exempt from Medicaid?

Usually no. Checking accounts, savings accounts, CDs, and similar cash assets are usually countable unless a specific rule applies.

Does life insurance count as an asset?

It depends on the type of policy and whether it has cash value. Illinois DHS gives the cash value of a nonexempt life insurance policy as an example of something that can be part of the asset limit.

What can a spouse keep if the other spouse goes into a nursing home?

In 2026, Illinois HFS says the Community Spouse Resource Allowance standard is $143,172. Illinois DHS also lists the 2026 CSRA at up to $143,172 for applications received on or after January 1, 2026.

Can I give money to my children before applying for Medicaid?

Gifts or transfers for less than fair market value can create a Medicaid penalty if made during the 5-year lookback period for long-term care Medicaid. Families should get advice before making transfers.

Is a trust protected from Medicaid?

A trust is not automatically protected. Revocable trusts usually do not protect assets from Medicaid. Some irrevocable trusts may help if they are drafted, funded, and timed correctly. The 5-year lookback period still matters.

What should I do before applying for Medicaid in Illinois?

Gather account statements, deeds, vehicle records, insurance policies, trust documents, income records, and any records of gifts or transfers. Then review the asset picture before applying, especially if a home, spouse, trust, or nursing home is involved.

Disclaimer:

The information provided in this article is for general educational and informational purposes only and does not constitute legal, financial, or tax advice. While based on Illinois law, Medicaid regulations frequently change. ElderSmart.net makes no representations or warranties as to the accuracy, completeness, or current suitability of this information for any purpose. You should consult a qualified attorney or financial professional regarding your specific situation.

Use of this website or communication with ElderSmart does not create an attorney-client relationship. Do not send confidential or sensitive information until such a relationship has been formally established in writing.

By using this site, you acknowledge and agree that ElderSmart.net and its affiliates are not liable for any losses, injuries, or damages arising from your reliance on the content provided. For more details, please review our full Terms of Use and Privacy Policy.

Martin Fogarty is the founder of ElderSmart and The Heartland Law Firm in Glenview, Illinois. With more than 30 years of experience, Martin helps families navigate elder law, Medicaid planning, estate planning, trusts, long-term care issues, and asset protection. Through ElderSmart, he focuses on giving Illinois families clear, practical guidance so they can make confident decisions during difficult moments.